A credit card skimmer is a hidden device criminals attach to payment hardware to steal card data, and in more advanced cases they use a shimmer between the chip and reader. The risk is broad: 61.3 million Americans experienced fraudulent charges in the past year, totaling about $6.1 billion in unauthorized purchases, while only 5% of fraudulent charges involved a physically lost or stolen card.

If you're an MSP, vCISO, or reseller, that matters because your clients probably still think of skimming as a consumer banking problem. It isn't. It shows up at gas pumps, ATMs, retail point-of-sale devices, and online checkout pages. A hidden device that steals card data can turn into chargebacks, customer trust issues, compliance headaches, and a long week of incident response for the businesses you support.

Title Tag: What Is a Credit Card Skimmer: Prevent Fraud in 2026

Meta Description: Learn what a credit card skimmer is, how skimming devices work, how MSPs can detect and prevent skimming fraud, and where pentesting helps protect PCI DSS, SOC 2, HIPAA, and compliance-driven clients.

Defining Credit Card Skimmers for MSPs

A credit card skimmer is typically a hidden hardware overlay or inline reader installed on ATMs, fuel pumps, or POS terminals to capture data from the card's magnetic stripe when the card is swiped. The stolen track data can include the cardholder name, card number, and expiration date, which criminals can reuse to create counterfeit cards or support unauthorized transactions, as explained in Capital One's overview of credit card skimmers.

For an MSP, the important part isn't just the definition. It's the business impact. If your client runs a storefront, manages payment terminals, supports field kiosks, or hosts an e-commerce checkout, skimming moves from “fraud awareness” into risk assessment, compliance, and operational resilience.

A lot of business owners still ask, what is a credit card skimmer, as if it's a niche gadget. In practice, it's a quiet way to siphon payment data while normal transactions keep flowing. That's why the fraud often isn't discovered until a statement, dispute, or bank alert forces the issue.

Why MSPs should care

Your clients won't judge the incident based on attack taxonomy. They care that customer cards were exposed, the payment environment was compromised, and someone should have seen the warning signs earlier.

That puts MSPs and vCISOs in a familiar spot:

- Retail and hospitality clients need practical checks on terminals and staff workflows

- Healthcare and professional services firms may not process much card data, but they still face HIPAA, trust, and breach-response pressure if front-desk devices are tampered with

- Compliance-focused clients need documented controls that support PCI DSS, SOC 2, and ISO 27001 programs

For a plain-language reference you can share with clients, Tagada's explanation of card skimming is useful because it frames the threat in business terms instead of pure consumer advice.

Practical rule: If a client accepts card payments, skimming belongs in the same conversation as endpoint hardening, phishing defense, and access control.

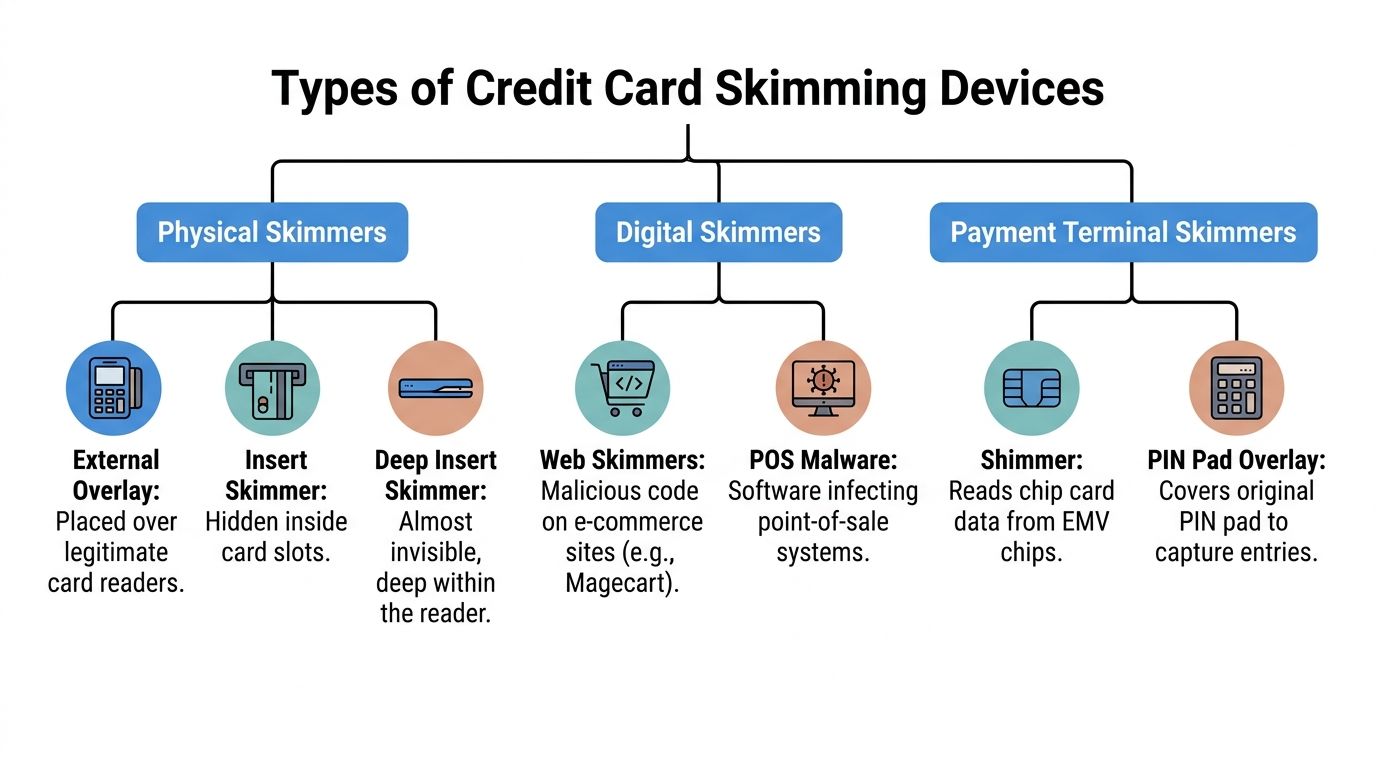

Exploring Different Types of Skimming Devices

Skimming isn't one device. It's a category of attacks. Some are physical, some are software-based, and some target the gap between modern chip cards and the terminals that read them.

Early in the conversation, it helps to show clients the threat environment visually.

Krebs on Security reported that skimming accounted for more than 80% of ATM fraud, and cited a U.S. Secret Service estimate that ATM fraud losses reached about $1 billion in 2008. More recently, compromised cards increased 368% from 2021 to 2022, and FICO reported a further 77% increase in cards impacted in the first half of 2023, totaling 120,000 cards, showing how the threat keeps evolving beyond the old ATM-only picture in Krebs' reporting on skimmers and ATM fraud.

Physical skimmers and overlays

The classic version is a fake reader placed over a real one. A customer swipes, the terminal appears to work, and the skimmer captures the stripe data on the way through.

Other physical variants sit deeper in the slot or inside fuel pump hardware. These are harder for staff to notice during a casual glance, which is why physical inspection routines matter.

Shimmers and payment terminal attacks

A shimmer is thinner and more specialized. Instead of acting like a bulky overlay, it sits between the chip card and the reader. That makes it a different problem from old-school magnetic stripe skimming.

Payment terminals can also be attacked around the edges. Fake PIN pad overlays, hidden cameras, and tampered enclosures often work together. The criminal isn't relying on one tool. They're building a workflow to capture enough data to make fraud useful.

Digital skimming and checkout theft

The online version is often called digital skimming or e-skimming. Instead of touching a physical terminal, the attacker injects malicious code into a payment page and steals card details during checkout.

For MSPs, this is the key trade-off to explain. A client can inspect every register in the store and still miss the website problem entirely. That's why vulnerability scanning alone isn't enough. Payment security needs review of web apps, third-party scripts, change control, and the way checkout pages behave under attack.

Digital skimming is the same criminal idea with a different delivery method. Steal card data while the transaction still looks normal.

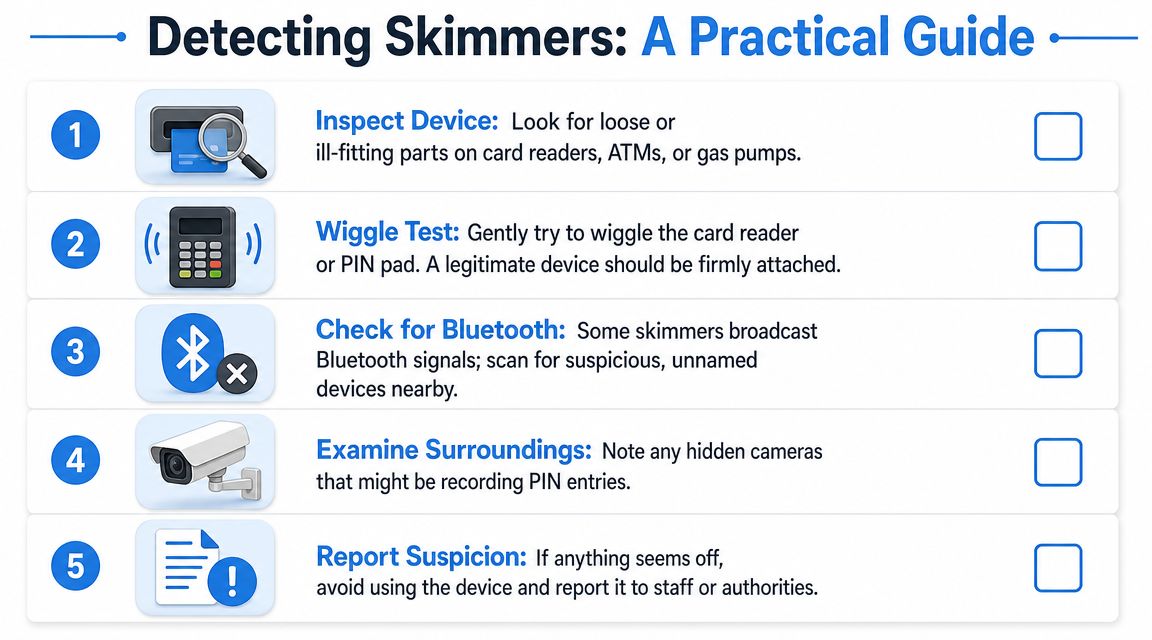

How to Detect Skimmers in the Wild

Most staff training on skimmers is too shallow. It says “look for anything unusual,” which sounds reasonable but doesn't help a cashier, store manager, or field technician make a decision under pressure.

A better approach is to give people a short checklist they can repeat. This graphic helps with that.

What staff can check physically

Start with the obvious because that catches more issues than people expect:

- Loose parts that don't match the rest of the terminal

- Different colors or textures around the card slot or keypad

- Bulkier reader faces than nearby terminals of the same model

- Tiny cameras aimed at the keypad

- Broken seals or disturbed panels on fuel pumps and kiosks

The simple “wiggle test” is still useful. A legitimate reader should feel firmly attached. If a faceplate shifts, lifts, or clicks strangely, stop using it.

What MSPs should check digitally

For online checkout systems, detection looks different. Watch for unauthorized JavaScript, changes to payment-page behavior, unexplained third-party script additions, and alerts from website monitoring or file integrity tools.

The role of user education is significant. If your clients need a stronger process for helping employees spot suspicious behavior, pair skimmer awareness with broader security awareness training guidance so staff understand when to escalate instead of guessing.

A short internal checklist works better than a policy binder. Keep it simple:

- Compare the device to another terminal nearby

- Touch the reader gently to check for movement

- Inspect the surroundings for cameras or odd attachments

- Stop transactions immediately if anything feels off

- Escalate to management and IT before anyone removes hardware

If a front-line employee feels rushed, they'll default to “it probably works.” Detection training has to make stopping the transaction the easier choice.

Proactive Prevention for Your Clients and Business

Detection is good. Prevention is cheaper.

The hard truth is that many businesses only think about skimming after a bank call or customer complaint. That mindset doesn't hold up well when card data is involved. USC Credit Union reported that 61.3 million Americans experienced fraudulent charges in the past year, and Mastercard reported that nearly three quarters of publicly disclosed breaches in 2022 involved digital skimming, which shows why prevention has to include both physical and online payment environments in any serious guide to combat card skimming.

Controls that actually help

A practical prevention plan usually includes a mix of people, process, and technical controls:

- Routine terminal inspections done by named staff, not “whoever is available”

- Tamper-evident measures on pumps, kiosks, and enclosures so changes are easier to spot

- Limited physical access to payment devices and back-office network gear

- Change monitoring on e-commerce pages, checkout scripts, and payment integrations

- Role-based access for staff who can update POS software or web content

This is also where good policy beats expensive theater. Fancy awareness posters won't help if nobody owns daily inspection, evidence handling, or vendor escalation.

Compliance pressure is real

For clients handling payment data, PCI DSS is the obvious conversation. But skimming incidents can also spill into SOC 2, ISO 27001, and broader GRC reviews because they expose weak physical controls, poor change management, and thin incident response.

Healthcare and mixed-use businesses add another layer. Even if the skimming issue starts with payment hardware and not protected health information, weak front-desk security still raises questions under HIPAA and general compliance hygiene.

A lot of smaller organizations need plain-English references, not just standards language. This short list of data security tips is useful for non-technical stakeholders who need simple habits reinforced alongside formal policy. For payment-focused environments, technical validation also matters. A targeted PCI compliance pentesting approach helps confirm whether the controls on paper hold up in practice.

What doesn't work well

Some defenses sound good and fail in practice:

- One-time inspections after a scare, then no repeat process

- Generic vulnerability scans used as a substitute for manual review

- Assuming chip cards solved skimming across every environment

- Treating the website and the storefront as separate risks when the brand impact is shared

The MSP opportunity is clear. Clients need an affordable, repeatable service model. Not a one-off panic purchase.

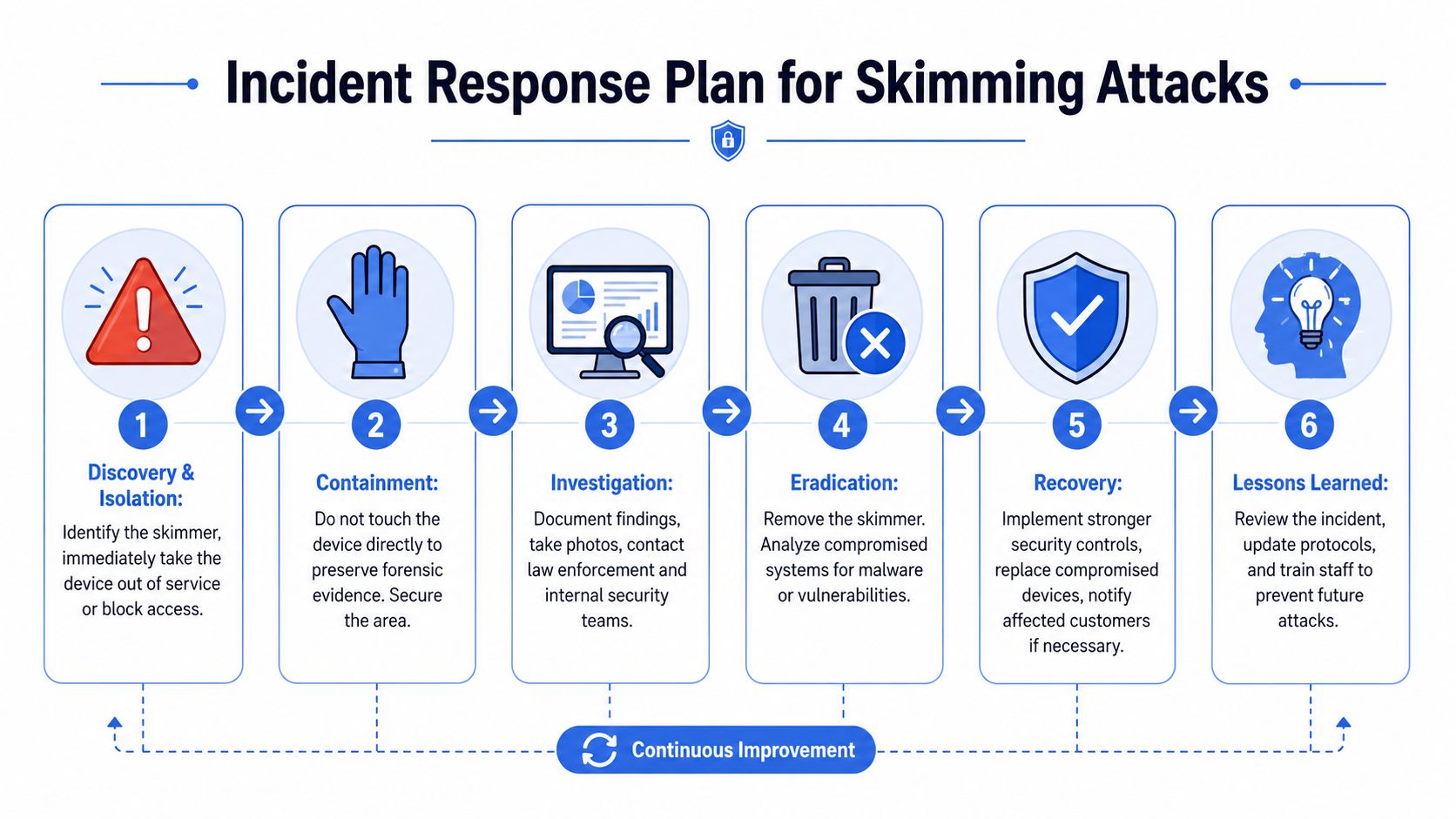

Your Incident Response Plan for Skimming Attacks

The moment a skimmer is found, people want to rip it off the machine and move on. That's understandable. It's also a mistake.

Many organizations prepare for prevention but not for the aftermath. Takoma Park's guidance notes that criminals often pair skimmers with hidden cameras or insider help, which turns a single device discovery into a broader fraud-chain problem that needs a coordinated response across environments in their explanation of how credit card skimming works.

First actions that matter

Start with containment. Take the terminal, pump, kiosk, or checkout workflow out of service. Block access before someone “tests” the device again and adds more exposure.

Then preserve evidence:

- Don't pull the device apart unless your process requires it

- Photograph the setup from multiple angles

- Document who found it and when

- Notify internal security, management, and law enforcement based on the client's plan

Scope and recovery

After containment, determine what else may be affected. If a physical skimmer is present, review nearby devices, camera angles, access logs, maintenance records, and who had access to the location. If the issue is digital, review recent code changes, script sources, admin access, and third-party integrations.

For compliance-minded clients, this is where documented response matters. SOC 2 and ISO 27001 programs both benefit from clear handling, evidence retention, root-cause analysis, and corrective action tracking.

A skimmer incident is rarely just a hardware cleanup task. It's an investigation, a communication event, and a control failure review.

The recovery step should end with a refreshed risk assessment, updated training, and new ownership for the controls that failed.

How Penetration Testing Uncovers Hidden Risks

Skimming sits at the intersection of physical security, payment workflows, web application security, and human behavior. That's exactly why a real penetration test is useful. A scanner can flag missing patches. It won't tell you whether a checkout page can be tampered with, whether staff can be socially engineered around a payment terminal, or whether physical controls around POS systems are weak enough to support fraud.

Where pentesting fits

A strong pentest, pen test, or broader penetration testing engagement can help uncover:

- Web checkout weaknesses that support digital skimming or script tampering

- POS and internal network exposure that could allow malware or unauthorized access

- Physical access gaps around terminals, kiosks, or back-office systems

- Social engineering paths that let attackers bypass process controls

- Reporting gaps that leave MSPs and vCISOs with poor evidence for compliance

This matters for PCI DSS, but it also supports broader compliance work tied to SOC 2, HIPAA, and ISO 27001. A real engagement should end with a useful report, not a giant export file no one reads.

Why channel partners need the right model

For MSPs, resellers, CPAs, and GRC firms, the challenge usually isn't awareness. It's delivery. Clients need affordable, fast, manual pentesting performed by people who know how attackers work. They also need a partner model that doesn't poach the account.

That channel-only model is where physical pentesting services and application-focused testing become practical. MSP Pentesting provides white label pentesting for partners, including manual pentests by OSCP, CEH, and CREST certified pentesters, so MSPs and vCISOs can deliver a branded risk assessment without creating a competitive conflict.

A good engagement doesn't just answer, what is a credit card skimmer. It answers the harder question your clients care about: where are we exposed, what should we fix first, and how fast can we prove progress?

If you support clients that process card payments, sell online, or need help tying skimming risk back to PCI DSS, SOC 2, HIPAA, or broader compliance work, MSP Pentesting can help you deliver white label pentest, pen testing, and penetration testing services under your brand. Contact us today to talk through an affordable scope, fast turnaround, and a channel-only partnership that supports your client relationships instead of competing with them.

.png)

.png)

.png)